Cutting power prices

By decoupling from gas and deploying wind and solar

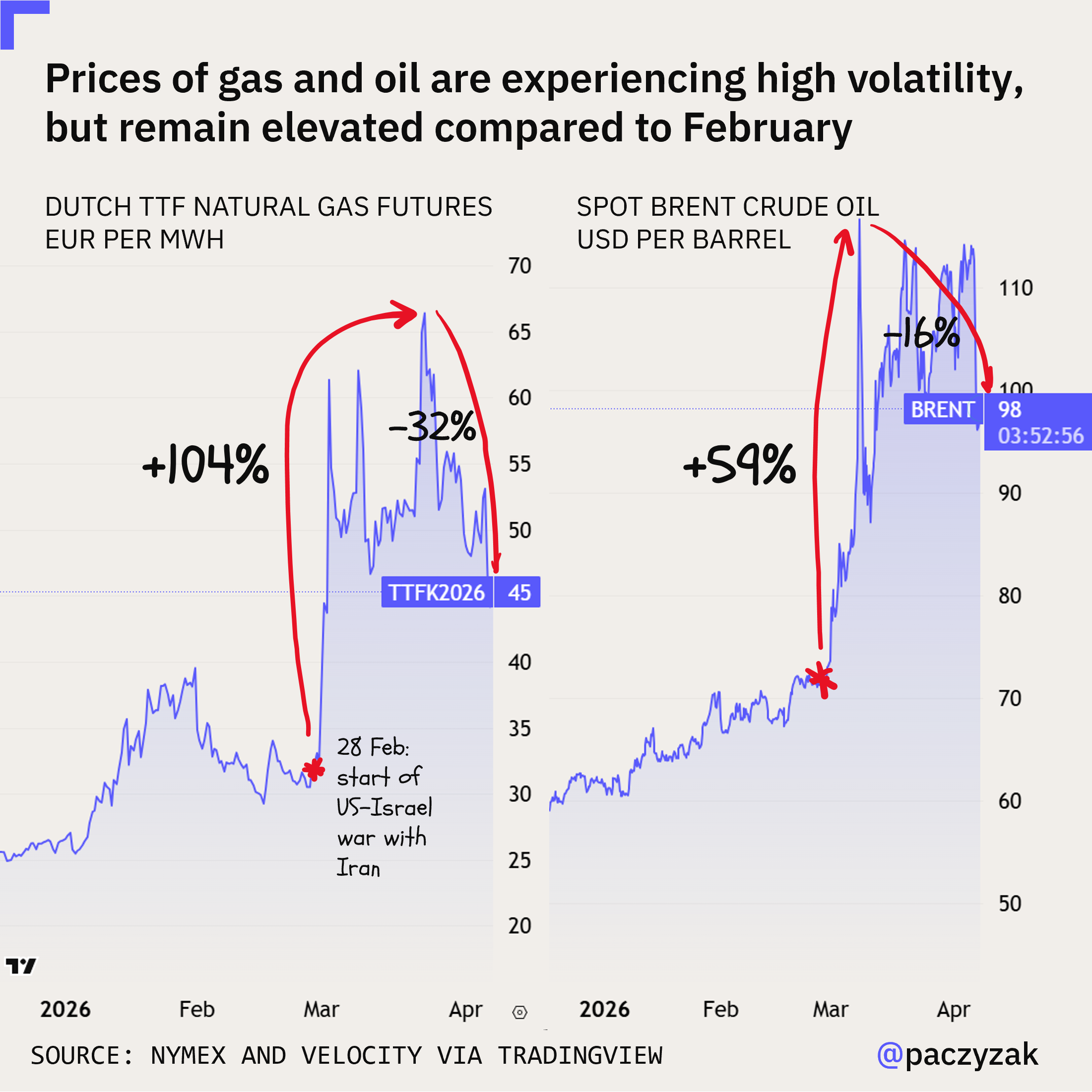

It’s been just over a month since the start of the US-Israel war with Iran on February 28. Immediately after the first air strikes, prices of oil skyrocketed to $117 per barrel, almost reaching the $131 record from 2022. After the 2-week ceasefire announced on April 7th, they went down to $98, but will likely stay volatile.

The price of diesel went beyond $200 per barrel in Europe contributing to a rapid cost increase in transport, agriculture, shipping, construction.

Natural gas prices noticed similar volatility, doubling from around €25-30 per MWh to €50-65, and then dropping to €45 on April 8.

Gas reliance = higher price shock exposure

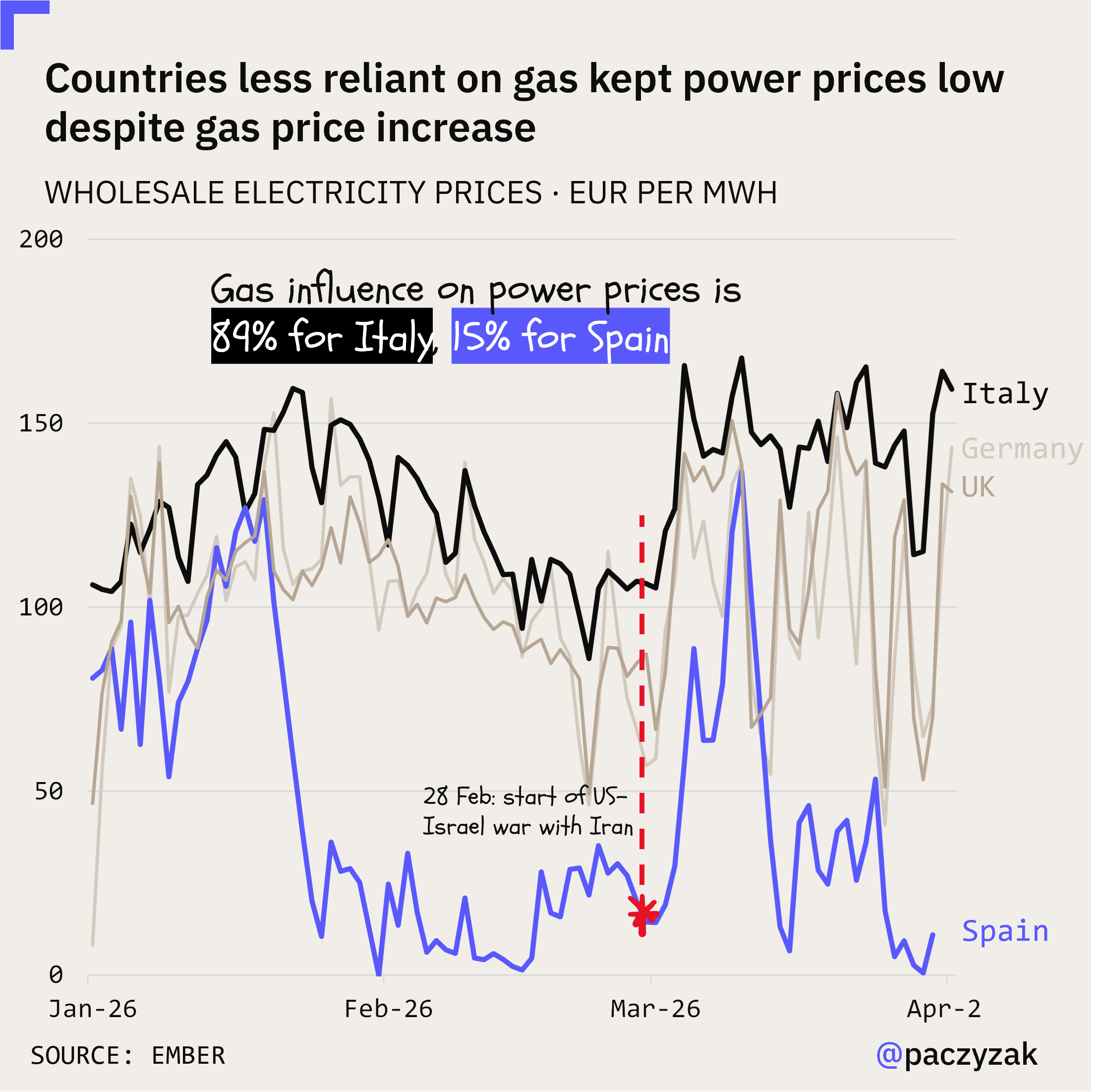

The rise in oil and gas prices translated to an almost overnight ~50% rise in electricity prices across Europe. Not all countries got hit the same though.

Ember’s early analysis of the developing energy crisis showed that countries with lower gas reliance, like Spain, are way more resilient. Thanks to the abundance of cheap wind and solar electricity (and a battery boom), Spain was able to almost immediately go back to low power prices after a brief shock. On the other side of the spectrum was Italy, where electricity prices are closely tied to gas, and remained among the highest in Europe throughout March.

In the first week of April 2026, Spain’s average price was €18 per MWh, Italy was €131 - a 7x gap. Of course there are other cost components to consider. But in total bill terms (with taxes, levies, network charges), Italian business paid 60% more than Spanish ones already in 2024, and that trend is unlikely to change.

UK: Wind and solar reduce gas import costs

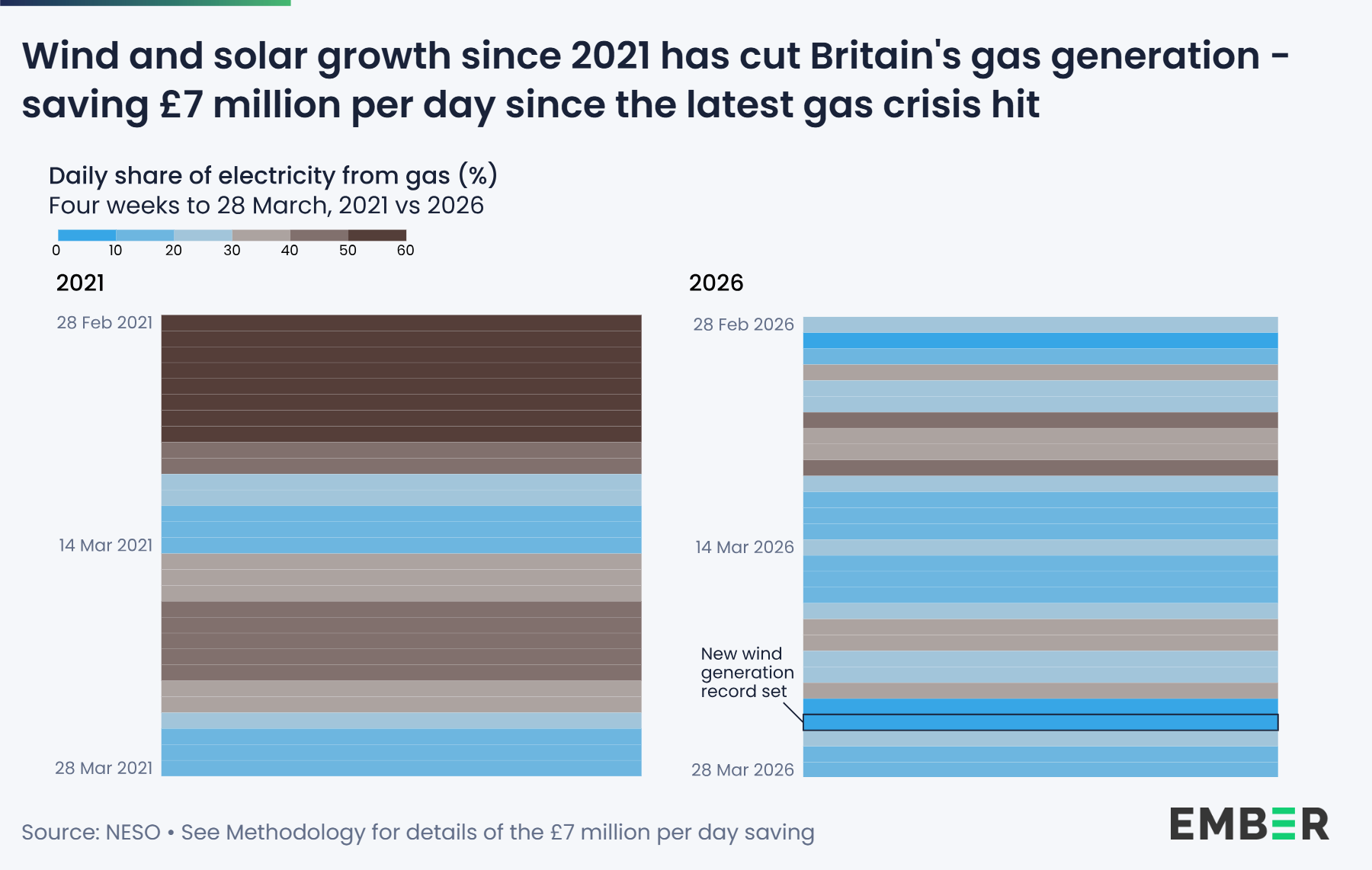

An interesting story is developing in the UK too, where over a quarter of the country’s total wind and solar capacity was deployed in just 5 years - since the last energy crisis in 2022. As a result, in March 2026 gas power generation was 39% lower than in March 2021, saving around £7 million per day in gas purchases. This was possible despite a 42% increase in gas prices compared to end of February. More in Ember’s latest report launched today.

Türkiye: Renewables cut electricity bills

Another example is Türkiye. According to a recent Ember report, in 2025 renewables cut total household electricity bills by 9% on average, and up to 17% in spring and summer months. Non-household consumers saw benefits too: on average $250,000 in annual savings for industry and $30,000 for commercial establishments thanks to renewables deployment.

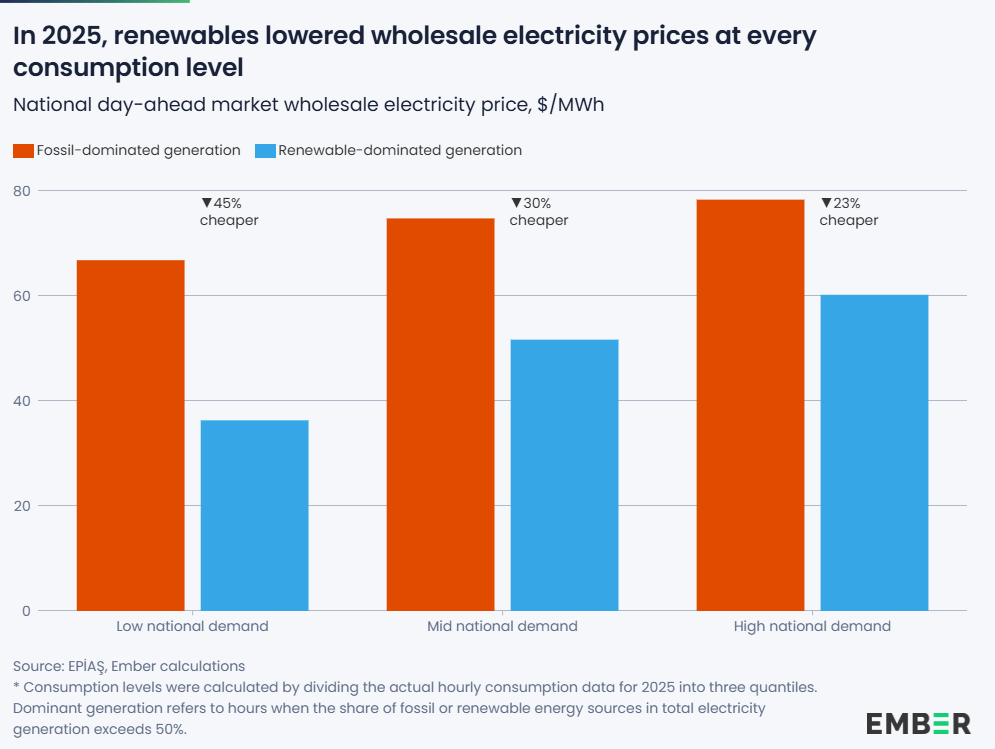

In wholesale terms, renewables cut prices by up to 45% during hours of low demand and high renewable generation. Even at high national demand moments, a 23% reduction was noticed - contributing to the lower bills for households and businesses.

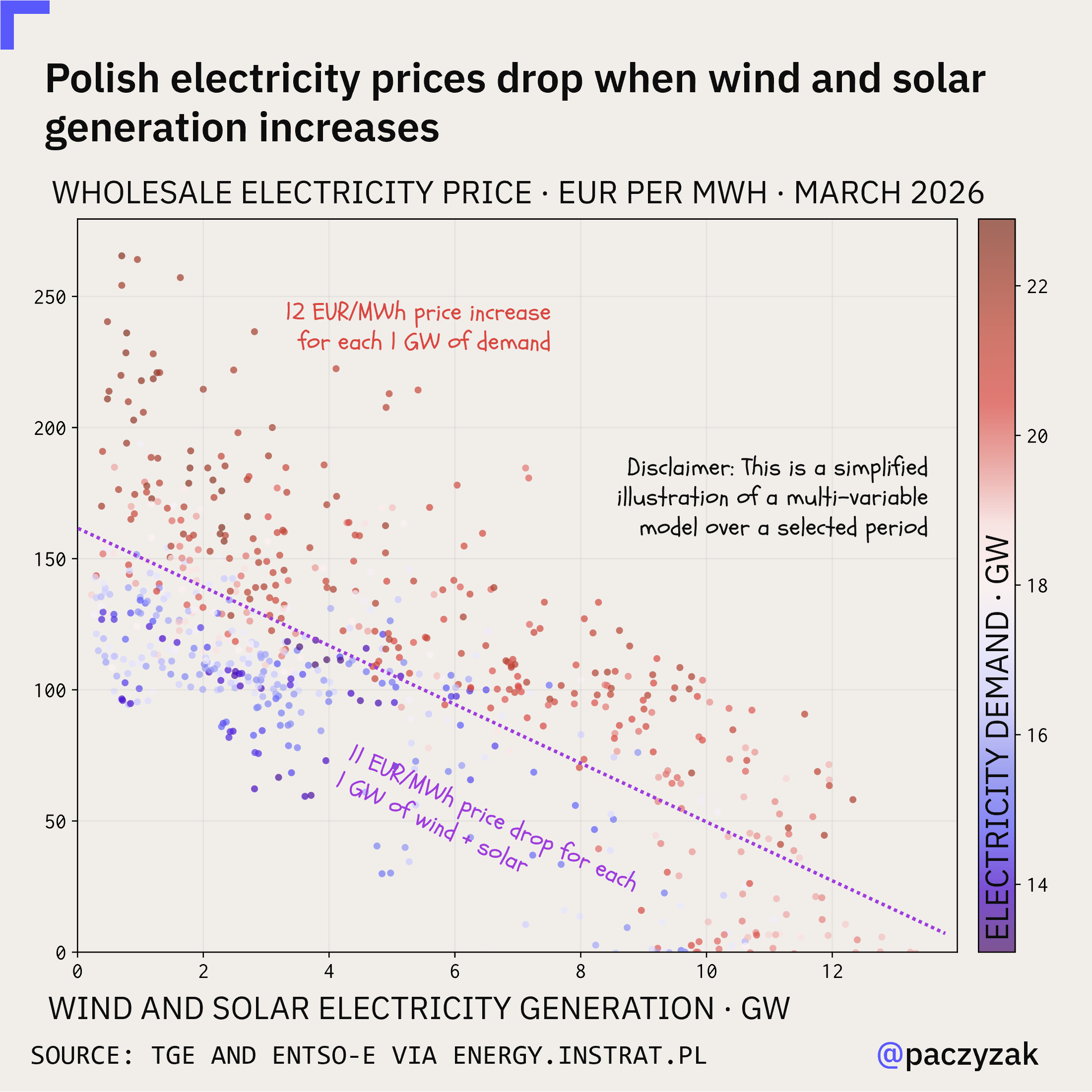

Poland: the more wind and solar, the lower the electricity price

And then there’s Poland. With prices typically shaped by coal rather than gas. But Poland is deploying new gas power plants, plus coal isn’t cheap either. The result is hardly surprising - some of the highest power prices in Europe.

There’s light in the tunnel though. Poland added 20 GW of solar capacity since mid-2021. And the more wind and solar in the system, the more gas and coal is pushed out, and the cheaper the electricity.

Looking at hourly data for 2026, each extra GW of wind and solar generation reduces the price by 11 EUR/MWh. On the other hand, each GW of demand adds 12 EUR/MWh. So best option would be to combine clean power with demand shifting through flexibility and storage. Not surprising, but nice to see in the numbers.

There’s again the question of other cost components. But network charges would be rising anyways - 40% of substations in Poland are over 40 years old. And a major chunk of Polish electricity bills is the capacity market - the vast majority of it subsidizing coal and gas…

The conclusion from all this: gas is quite unpredictable and it’s hard to see how it could ever become cheap. Fortunately, clean power can help decouple electricity prices from gas, shielding countries and consumers from the costs and the volatility.

Geeky disclaimer: I tested a few econometric models over Jan-April hourly data, verified positive Granger causality. Also added pre-/post-war dummy variables, adjusted for time of day and week, split wind and solar, tested with lags (long-term effects remain consistent). Will probably add gas and coal SRMCs at some point. If you have questions, let me know in the comments or on LinkedIn.

Thanks for reading!

If you’d like to get similar stories every Wednesday (sometimes Thursday :P), subscribe below.

The methodology disclosure at the end is what sets this apart. Granger causality with war dummies and lag tests is more rigor than most paid research bothers with.

One pushback on the interpretation, though. The wholesale decoupling story holds. Spain’s €18/MWh week is real, and the merit-order mechanism is well-documented. But if you look at retail household prices across the same period, the Iberian gap compresses dramatically. Eurostat H1 2025 puts Spain at €26.1/100 kWh against an EU average of €28.72, roughly 9% below, despite a wholesale gap the chart shows as 7x against Italy. Most of the decoupling effect disappears somewhere between the spot market and the household invoice.

The straightforward reading is that network and system charges are absorbing the wholesale saving upstream of retail. Constraint costs, must-run thermal dispatch for inertia and voltage support, capacity payments, ancillary services, transmission build-out. None of these shrink as renewable penetration rises, and several grow. The wholesale saving is real, but it is captured before it reaches the consumer’s bill.

Which leaves a distributional picture worth naming directly. Consumers see very little of the benefit in their monthly bills. Merchant generators absorb most of the cost through lower capture prices and compressed margins, and that compression is structural. It deepens as penetration rises rather than stabilizing. Ancillary and balancing markets are often pointed to as the recovery channel, but margins there are thin and the addressable market is small relative to the energy revenue being eroded. It’s not a plausible compensation mechanism for what’s being lost on the energy side.

The usual counter is the ETS angle, that carbon pricing either rewards low-emission generation or returns value through auction revenue. Both are real, but neither changes the picture in the way the counter implies. Auction revenue accrues to governments, not to consumers or merchant generators. And the emissions cost avoided by displacing gas is fundamentally a cost-suppression effect. It prevents the carbon component of electricity from escalating as allowance prices climb, but it doesn’t generate new value. It caps downside. A mechanism that caps downside is not the same as one that creates upside, and conflating the two is how the “everyone wins” framing survives scrutiny it probably shouldn’t.

Stack these together and the decoupling narrative reads less like “wholesale and retail both fall” and more like “wholesale value is redistributed away from generators without meaningfully reaching consumers, while system costs rise in parallel.” That’s a harder story to tell, but I think it’s closer to what the data is showing.

How do solar developers receive revenue? Are they solely reliant on the wholesale prices and therefore their revenue is the solar capture price of the wholesale price? Or do they receive fixed tariffs. If the latter where does that show up in the electricity bill?